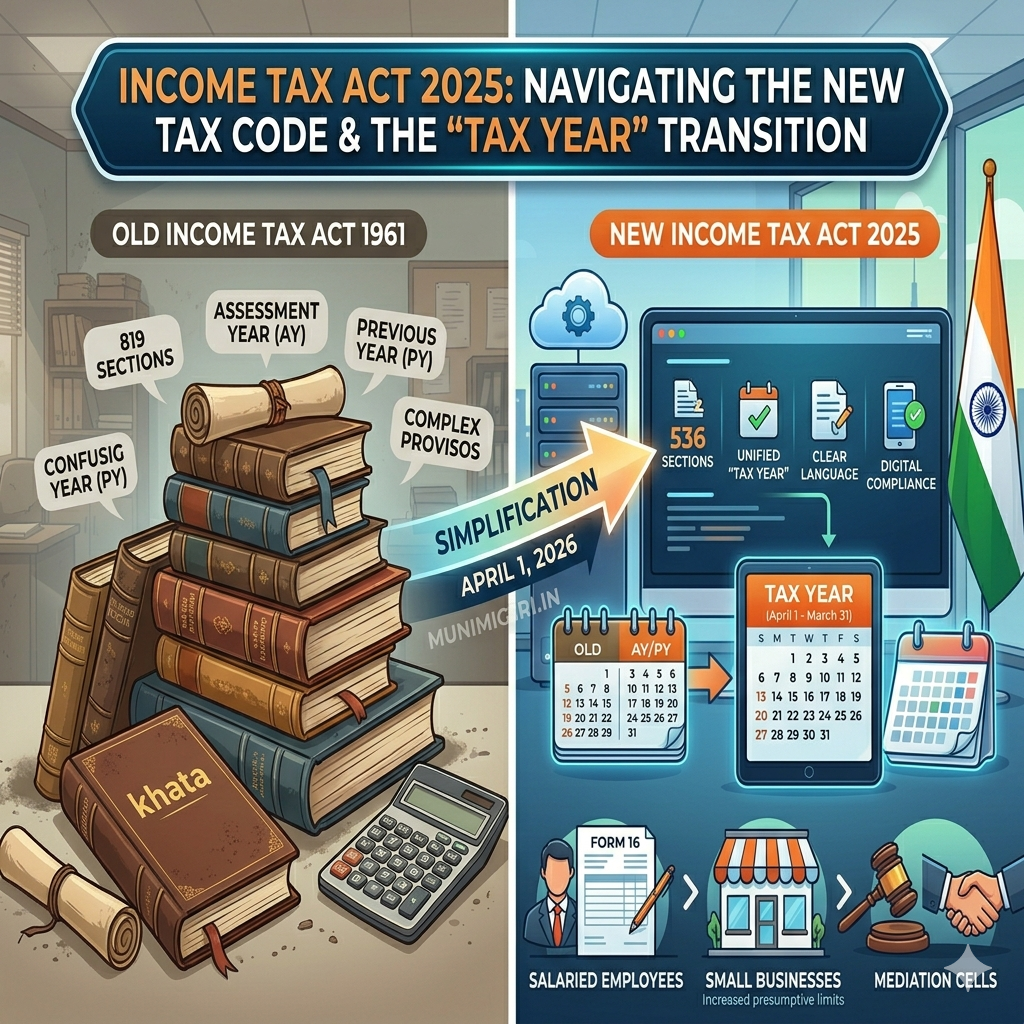

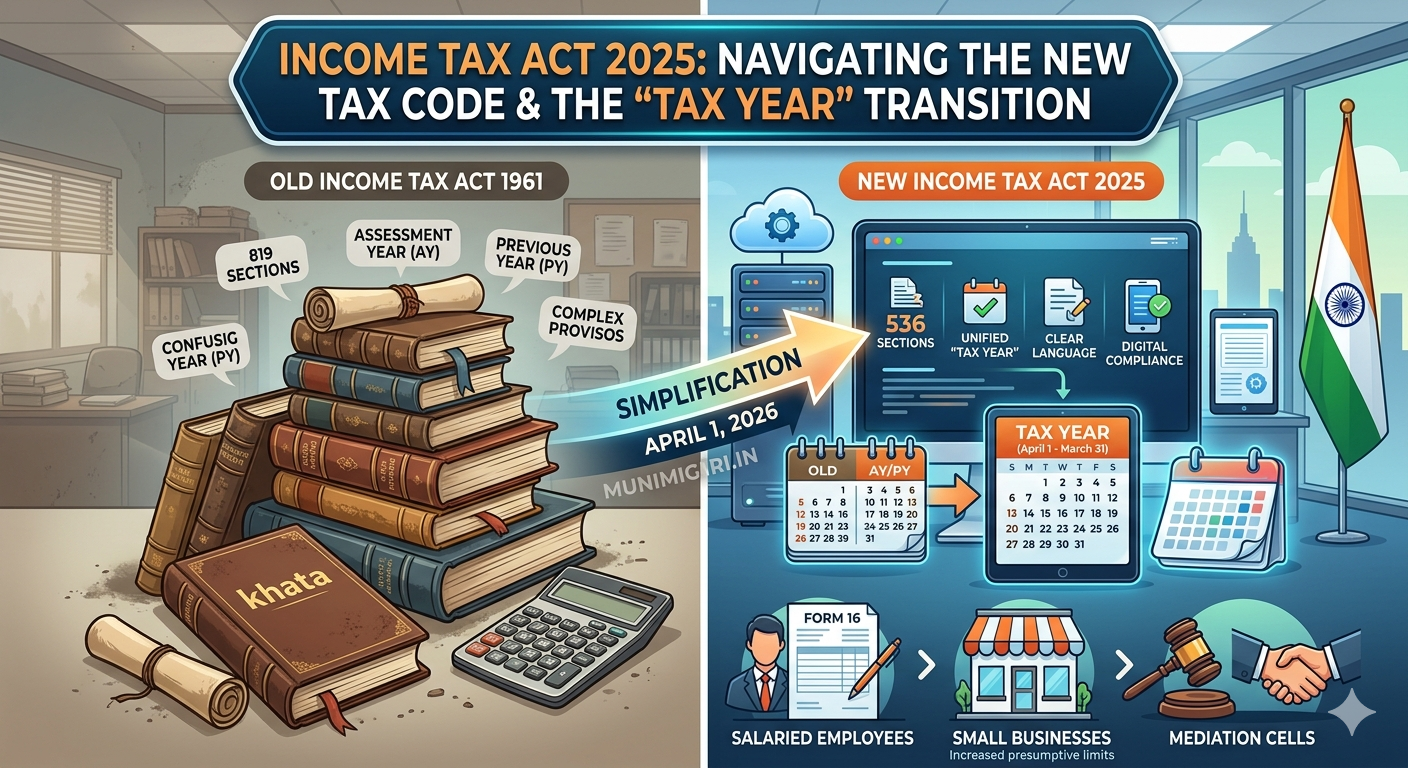

For over sixty years, the financial backbone of India was the Income Tax Act of 1961. While it served the nation through its transition into a global economy, it eventually became a behemoth of complexity, featuring over 800 sections and thousands of sub-clauses that required expert intervention for even basic understanding.

As of April 1, 2026, that era has officially ended. The Income Tax Act 2025 is now the law of the land. This isn’t just a “patch” or an amendment; it is a complete replacement of the old code. The primary objective? To reduce litigation, simplify language, and align Indian taxation with 21st-century digital realities.

One of the most radical shifts in this new act is the elimination of the dual-timing system—the “Previous Year” and “Assessment Year”—in favor of a single, unified “Tax Year.” In this comprehensive guide, Munimigiri breaks down every detail you need to know to stay compliant and tax-savvy in 2026.

The Death of “Assessment Year” (AY) vs. “Previous Year” (PY)

Historically, the Indian tax system operated on a “lag.” You earned money in one year (the Previous Year) and were assessed on it in the next (the Assessment Year). This terminology often confused non-professionals.

The Unified Tax Year Concept

Under the Income Tax Act 2025, the concept of “Assessment Year” has been abolished. We now move to a Tax Year (TY) system.

-

The Definition: A Tax Year is the period of 12 months commencing on the 1st day of April and ending on the 31st day of March.

-

The Application: If you earn a salary between April 2026 and March 2027, you are earning in Tax Year 2026-27. When you file your return in July 2027, you are filing for Tax Year 2026-27.

This alignment removes the mental gymnastics previously required. It streamlines accounting software, simplifies corporate reporting, and makes international tax comparisons much easier for the Income Tax Department (ITD).

Why the 1961 Act Had to Go

The old Act was a victim of its own longevity. Every year, Finance Ministers added layers of complexity via the Annual Finance Acts. By 2024, the Act was described by many legal experts as “unreadable.”

The “Clean Slate” Philosophy

The 2025 Act focuses on “Taxpayer First” principles:

-

Reduction in Sections: The Act has been compressed from 819 sections to 536 sections.

-

Removal of Provisos: The “provided that” culture has been minimized. Most conditions are now baked directly into the main sections.

-

Modern Terminology: Terms like “Assesse” have been largely replaced with “Taxpayer,” and “Direct Taxes” are now more clearly categorized into modern income streams like Virtual Digital Assets (VDA) and Gig Economy earnings.

Structural Changes: The New Section 4

Section 4 has always been the “Charging Section” of the Income Tax Act—the engine that gives the government the power to collect tax. In the Income Tax Act 2025, Section 4 has been completely re-engineered.

It now explicitly lists the five pillars of taxation:

-

The Person: Who is liable.

-

The Income: What is being taxed.

-

The Rate: Set by the annual Finance Act.

-

The Period: The newly defined Tax Year.

-

The Residence: Simplified criteria for Resident, Non-Resident, and Not-Ordinarily Resident (NOR).

Impact on Different Taxpayer Categories

A. Salaried Individuals

For the millions of salaried employees in cities like Mumbai, Bangalore, and Delhi, the transition is designed to be seamless.

-

Standard Deduction: The standard deduction has been restructured and is now linked to the “Tax Year” inflation index.

-

Employer Compliance: Employers will now issue Form 16 based on the “Tax Year,” ensuring that the TDS (Tax Deducted at Source) matches the reporting year perfectly.

B. Small Business & Professionals (The “Munimi” Segment)

Small business owners in local markets—from the textile hubs of Surat to the tech startups in Hyderabad—will benefit from the expanded Presumptive Taxation limits. Under the 2025 Act, the threshold for presumptive tax for professionals has been simplified, and the “Audit” requirements have been raised to reduce the compliance burden on SMEs.

C. Non-Resident Indians (NRIs)

The 2025 Act clarifies the “182-day rule” and introduces a more robust mechanism for claiming Double Taxation Avoidance Agreement (DTAA) benefits directly through the e-filing portal, reducing the need for manual physical submissions at international tax offices.

Changes in TDS and Compliance Procedures

The Income Tax Act 2025 has consolidated nearly 40 different TDS sections into 15 broad categories. This is a massive relief for accounts departments across India.

-

Unified TDS Thresholds: Instead of different limits for rent, professional fees, and commissions, the Act moves toward a more uniform threshold for domestic payments.

-

Lowered Penalty for Minor Errors: Recognizing that digital errors happen, the 2025 Act introduces a “Cure Period” of 15 days for minor TDS mismatches before penalties are triggered.

The New Appeals and Dispute Resolution Mechanism

One of the biggest pain points in the Indian tax system was the duration of litigation. The new Act introduces:

-

Faceless 2.0: An improved version of the faceless assessment system with mandatory video conferencing options for complex cases.

-

Mediation Cells: Before going to the Income Tax Appellate Tribunal (ITAT), taxpayers can now opt for a Mediation Cell to settle disputes involving amounts under ₹50 lakhs, potentially clearing millions of pending cases.

Digital Assets and the Modern Economy

The 1961 Act struggled to keep up with Crypto and NFTs. The Income Tax Act 2025 treats Virtual Digital Assets (VDAs) as a distinct category of “Modern Income.”

-

Uniform 30% Tax: The 30% tax on VDA gains remains, but the 2025 Act provides clearer rules on “set-off” losses between different types of digital assets, which was a major bone of contention in previous years.

Geographic Context (GEO): What it means for Local Taxpayers

Whether you are filing from the heart of New Delhi, managing a business in Punjab, or handling exports from Tamil Nadu, the 2025 Act applies uniformly across India. However, the Department is setting up Regional Ease-of-Compliance Centers in major Tier-2 cities to help local “Munimis” and accountants transition from the old 1961 terminology to the new 2025 code.

Important Deadlines for Tax Year 2026-27

Mark your calendars, as the 2025 Act has slightly adjusted the filing calendar:

-

August 31, 2027: The new deadline for individual taxpayers (non-audit).

-

October 31, 2027: The deadline for businesses requiring an audit.

-

December 31, 2027: The last date for “Updated Returns” (the new version of Belated Returns).

Transitioning Your Accounts: A Checklist for 2026

To ensure you don’t fall foul of the new law, Munimigiri recommends the following steps:

-

Update Software: Ensure your accounting software (like Tally or Zoho) is updated to support the “Tax Year” nomenclature.

-

Re-map Sections: Update your internal TDS charts to reflect the new 536-section numbering.

-

Audit Old Records: Remember that for any income earned before April 1, 2026, the 1961 Act rules still apply. Keep those records separate.

-

Educate Your Team: Ensure your finance team understands that “AY 2027-28” is a term of the past; it is now simply TY 2026-27.

Conclusion

The Income Tax Act 2025 is a monumental step toward “Minimum Government, Maximum Governance.” By stripping away the linguistic baggage of the 1960s and focusing on a unified Tax Year, the Indian government has made the tax system more transparent, digital-friendly, and accessible.

At Munimigiri, we believe that knowledge is the best tax-saving tool. Understanding these structural changes early will help you avoid penalties and plan your investments more effectively for the years to come.

Summary Table: 1961 Act vs. 2025 Act

| Feature | Income Tax Act, 1961 | Income Tax Act, 2025 |

| Primary Period | Previous Year & Assessment Year | Unified Tax Year |

| Total Sections | 819 | 536 |

| Complexity | High (1200+ Provisos) | Moderate (Simplified Language) |

| Digital Assets | Added as amendments | Integrated as Core Income |

| Dispute Resolution | Lengthy Tribunal process | Mediation Cells + Faceless 2.0 |

Frequently Asked Questions (FAQs)

Q1: Will my pending tax refund from 2024 be affected by the new Act?

No. Any refund or assessment pertaining to years prior to April 1, 2026, will be processed under the provisions of the old Income Tax Act, 1961.

Q2: Does the “Tax Year” change the dates of the Financial Year?

No. The period remains April 1st to March 31st. Only the name and the assessment logic have changed to be more intuitive.

Q3: Are tax rates lower in the 2025 Act?

The Act defines the structure of the law. The actual rates (the percentages you pay) are still determined by the annual Finance Act/Budget. However, the simplified rules may lead to lower compliance costs for businesses.

Q4: Is the new Act applicable to all of India?

Yes, the Income Tax Act 2025 is a central law and applies to all states and union territories of India.